Evaluating statistical audit samples

Koen Derks

Source:vignettes/articles/sample-evaluation.Rmd

sample-evaluation.RmdIntroduction

Welcome to the ‘Evaluating statistical audit samples’ vignette of the

jfa package. This page demonstrates how to evaluate the

misstatement in an audit sample using the evaluation()

function in package.

In auditing, the objective of evaluation is typically 1) to estimate the misstatement in the population based on a sample or 2) to test the misstatement against a critical upper limit, known as performance materiality.

Required information

Firstly, to evaluate an audit sample using the

evaluation() function, the sample data must be available in

one of two formats:

-

Summary statistics: This includes (a vector of) the

number of items (

n), (a vector of) the sum of misstatements/taints (x) and optionally (a vector of) the number of units in the population (N.units). -

Data: A

data.framethat contains a numeric column with book values (values), a numeric column with audit (i.e., true) values (values.audit), and optionally a factor column indicating stratum membership (strata).

By default, evaluation() estimates the population

misstatement and returns a point estimate as well as a

confidence/credible interval around this estimate, expressed as a

percentage (conf.level

100). However, in audit sampling, the population is typically subject to

a certain maximum tolerable misstatement defined by the performance

materiality

.

You can provide the performance materiality to the

evaluation() function as a fraction using the

materiality argument. In addition to the default

estimation, specifying a value for materiality triggers the

comparison of two competing hypotheses. The hypotheses being compared

depend on the input for the alternative argument.

-

alternative = "less"(default): versus -

alternative = "greater": versus -

alternative = "two.sided": versus

Once the auditor has established the materiality (if applicable), they must make a decision on whether to stratify the population. Stratification is the process of dividing the population into smaller subgroups that contain similar items, referred to as strata, and selecting a sample from each stratum. In the following sections, we will demonstrate how to evaluate statistical audit samples, both stratified and non-stratified.

Evaluation using summary statistics

We first consider the scenario where the auditor does not have access to the sample data and wants to perform inference about the misstatement using summary statistics from the sample.

Non-stratified samples

In a non-stratified sampling approach, the auditor does not divide the population into different strata. This approach might be suitable when the auditor is auditing the general ledger of a small business and has substantiated that the population comprises homogeneous items, such as all items being employment contracts subject to a shared ensemble of control systems.

Classical approach

Classical hypothesis testing employs the p-value to determine whether to reject the null hypothesis of material misstatement . For instance, let’s assume an auditor aims to confirm if the population contains less than five percent misstatement. This suggests the hypotheses : 0.05 and : 0.05. The auditor selects a sample of = 100 items, with = 1 item containing a misstatement. They establish the significance level for the p-value (i.e., the sampling risk) at = 0.05, indicating that a p-value below 0.05 will suffice to reject the null hypothesis. The following command evaluates the sample using a classical non-stratified evaluation method (Stewart, 2012).

evaluation(materiality = 0.05, x = 1, n = 100)##

## Classical Audit Sample Evaluation

##

## data: 1 and 100

## number of errors = 1, number of samples = 100, taint = 1, p-value =

## 0.040428

## alternative hypothesis: true misstatement rate is less than 0.05

## 95 percent confidence interval:

## 0.00000000 0.04743865

## most likely estimate:

## 0.01

## results obtained via method 'poisson'The output indicates that the most likely misstatement in the population is estimated to be = = 0.01, or 1 percent, and the 95 percent (one-sided) confidence interval spans from 0 percent to 4.74 percent. It also reveals that the p-value is below 0.05, suggesting that the null hypothesis should be rejected. Consequently, the auditor can infer that the sample provides sufficient evidence to conclude with a reasonable degree of certainty that the population does not contain material misstatement.

Bayesian approach

Bayesian hypothesis testing employs the Bayes factor, either

or

,

to quantify the evidence that the sample provides in support of either

of the two hypotheses

or

(Derks et al., 2024). For instance, a

Bayes factor value of

= 10 (provided by the evaluation() function) can be

interpreted as the data being 10 times more likely under the hypothesis

of tolerable misstatement

than under the hypothesis of material misstatement

.

A value of

1 indicates evidence in favor of

and opposing

,

while a value of

1 indicates evidence supporting

and contradicting

.

The evaluation() function returns the value for

,

but

can be calculated as

.

Consider the earlier example where an auditor wishes to confirm if the population contains less than five percent misstatement, suggesting the hypotheses : 0.05 and : 0.05. They have selected a sample of = 100 items, with = 1 item found to contain a misstatement. The prior distribution is presumed to be a default beta(1,1) prior. The subsequent call evaluates the sample using a Bayesian non-stratified evaluation procedure (Derks et al., 2021; Stewart, 2013).

evaluation(materiality = 0.05, x = 1, n = 100, method = "binomial", prior = TRUE)##

## Bayesian Audit Sample Evaluation

##

## data: 1 and 100

## number of errors = 1, number of samples = 100, taint = 1, BF₁₀ = 515.86

## alternative hypothesis: true misstatement rate is less than 0.05

## 95 percent credible interval:

## 0.00000000 0.04610735

## most likely estimate:

## 0.01

## results obtained via method 'binomial' + 'prior'The output indicates that the most likely misstatement in the

population is estimated to be

=

= 0.01, or 1 percent, and the 95 percent (one-sided) credible interval

spans from 0 percent to 4.61 percent. The minor discrepancy between the

classical and default Bayesian results in the upper limit can be

attributed to the prior distribution, which needs to be proper for the

calculation of a Bayes factor. Classical results can be replicated by

formulating an improper prior distribution using

method = "strict" in the auditPrior()

function. The Bayes factor in this scenario is demonstrated to be

= 515, signifying that the sample data are approximately 515 times more

likely to occur under the hypothesis of tolerable misstatement than

under the hypothesis of material misstatement.

It is important to note that this is a considerably high Bayes factor

given the small amount of data observed. This can be explained by the

fact that the Bayes factor is influenced by the prior distribution for

.

The default prior distribution is not a good prior for

hypothesis testing. As a general guideline, when the prior distribution

is extremely conservative in relation to the hypothesis of tolerable

misstatement (as with method = 'default'), the Bayes factor

tends to overstate the evidence supporting this hypothesis. This

dependency can be alleviated by employing a prior distribution that is

impartial towards the hypotheses (Derks et al.,

2022a), which can be achieved using

method = "impartial" in the auditPrior()

function.

prior <- auditPrior(materiality = 0.05, method = "impartial", likelihood = "binomial")

evaluation(materiality = 0.05, x = 1, n = 100, prior = prior)##

## Bayesian Audit Sample Evaluation

##

## data: 1 and 100

## number of errors = 1, number of samples = 100, taint = 1, BF₁₀ = 47.435

## alternative hypothesis: true misstatement rate is less than 0.05

## 95 percent credible interval:

## 0.00000000 0.04110834

## most likely estimate:

## 0.0088878

## results obtained via method 'binomial' + 'prior'The output reveals that = 47, suggesting that under the presumption of impartiality, there is substantial evidence for , the hypothesis that the population contains misstatements less than five percent of the population (tolerable misstatement). Given that both prior distributions resulted in persuasive Bayes factors, the results can be deemed robust to the selection of prior distribution. Consequently, the auditor can deduce that the sample provides compelling evidence to conclude that the population does not contain material misstatement.

Stratified samples

In a stratified sampling method, the auditor extracts samples from various subgroups, or strata, within a population. This could be applicable in a group audit scenario where the audited organization comprises different components or branches. Stratification becomes pertinent for the group auditor when they need to form an opinion on the group as a whole, as they are required to consolidate the samples taken by the component auditors.

For instance, consider the retailer data set included in

the package. The organization in question has twenty branches spread

across the country. In each of the twenty strata, a component auditor

has conducted a statistical sample and reported the results to the group

auditor.

## stratum items samples errors

## 1 1 5000 300 21

## 2 2 5000 300 16

## 3 3 5000 300 15

## 4 4 5000 300 14

## 5 5 5000 300 16

## 6 6 5000 150 5

## 7 7 5000 150 4

## 8 8 5000 150 3

## 9 9 5000 150 4

## 10 10 5000 150 5

## 11 11 10000 50 2

## 12 12 10000 50 3

## 13 13 10000 50 2

## 14 14 10000 50 1

## 15 15 10000 50 0

## 16 16 10000 15 0

## 17 17 10000 15 0

## 18 18 10000 15 0

## 19 19 10000 15 1

## 20 20 4000 15 3Generally, there are two methodologies for evaluating a stratified

sample: no pooling and partial pooling (see Derks

et al., 2022b). When using the evaluation() function

in a stratified sampling context, you need to specify the type of

pooling to be used via its pooling argument. No pooling

presumes no similarities between strata, implying that all strata are

analyzed independently. Partial pooling presumes both differences and

similarities between strata, implying that information can be shared

between strata. This technique is also known as multilevel or

hierarchical modeling and can lead to more efficient population and

stratum estimates. However, it is currently only available in

jfa when conducting a Bayesian analysis. For this

reason, this vignette primarily describes the Bayesian approach to

evaluating stratified audit samples. However, transitioning from a

Bayesian approach to a classical approach only requires setting

prior = FALSE.

The number of units (this can be items or monetary units depending on

the audit objective) per stratum in the population can be supplied with

N.units to weigh the stratum estimates for determining the

population estimate. This process is known as poststratification. If

N.units is not specified, it is assumed that each stratum

is equally represented in the population.

Approach 1: No pooling

The no pooling approach (pooling = "none") is the

default option and assumes there are no similarities between strata.

This implies that the prior distribution, specified through

prior, is applied independently in each stratum. This

approach allows for independent estimates of the misstatement in each

stratum, but for this reason it also results in a relatively high

uncertainty in the population estimate. The following command evaluates

the sample using a Bayesian stratified evaluation procedure, where the

stratum estimates are poststratified to derive the population estimate.

Note that it is important to set the seed via set.seed()

because the posterior distribution is determined via sampling.

set.seed(1)

result_np <- evaluation(

materiality = 0.05, method = "binomial",

n = retailer[["samples"]], x = retailer[["errors"]],

N.units = retailer[["items"]], pooling = "none",

alternative = "two.sided", prior = TRUE

)

summary(result_np)##

## Bayesian Audit Sample Evaluation Summary

##

## Options:

## Confidence level: 0.95

## Population size: 144000

## Materiality: 0.05

## Hypotheses: H₀: Θ = 0.05 vs. H₁: Θ ≠ 0.05

## Method: binomial

## Prior distribution: Nonparametric

##

## Data:

## Sample size: 2575

## Number of errors: 115

## Sum of taints: 115

##

## Results:

## Posterior distribution: Nonparametric

## Most likely error: 0.0598

## 95 percent credible interval: [0.042763, 0.082201]

## Precision: 0.022401

## BF₁₀: 0

##

## Strata (20):

## N n x t mle lb ub precision

## 1 5000 300 21 21 0.07000 0.04637 0.10467 0.03467

## 2 5000 300 16 16 0.05333 0.03324 0.08489 0.03156

## 3 5000 300 15 15 0.05000 0.03069 0.08086 0.03086

## 4 5000 300 14 14 0.04667 0.02816 0.07681 0.03014

## 5 5000 300 16 16 0.05333 0.03324 0.08489 0.03156

## 6 5000 150 5 5 0.03333 0.01472 0.07558 0.04225

## 7 5000 150 4 4 0.02667 0.01084 0.06643 0.03977

## 8 5000 150 3 3 0.02000 0.00726 0.05696 0.03696

## 9 5000 150 4 4 0.02667 0.01084 0.06643 0.03977

## 10 5000 150 5 5 0.03333 0.01472 0.07558 0.04225

## 11 10000 50 2 2 0.04000 0.01230 0.13459 0.09459

## 12 10000 50 3 3 0.06000 0.02178 0.16242 0.10242

## 13 10000 50 2 2 0.04000 0.01230 0.13459 0.09459

## 14 10000 50 1 1 0.02000 0.00478 0.10447 0.08447

## 15 10000 50 0 0 0.00000 0.00050 0.06978 0.06978

## 16 10000 15 0 0 0.00000 0.00158 0.20591 0.20591

## 17 10000 15 0 0 0.00000 0.00158 0.20591 0.20591

## 18 10000 15 0 0 0.00000 0.00158 0.20591 0.20591

## 19 10000 15 1 1 0.06667 0.01551 0.30232 0.23565

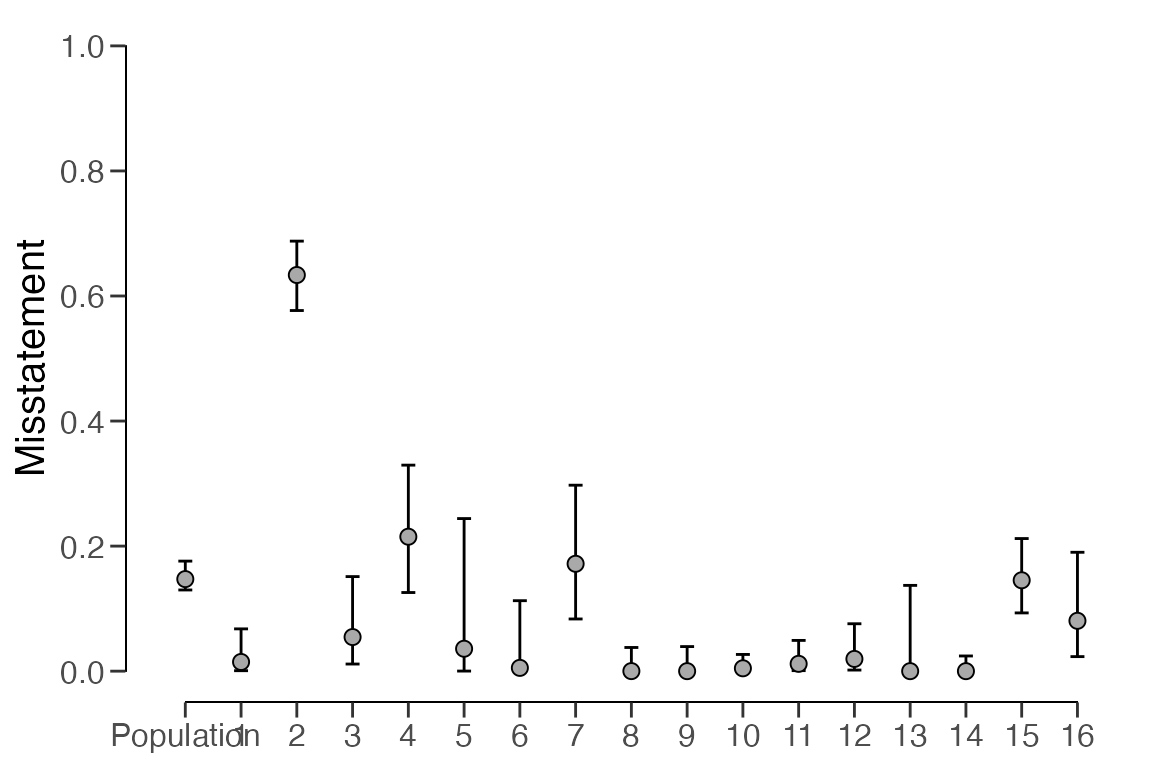

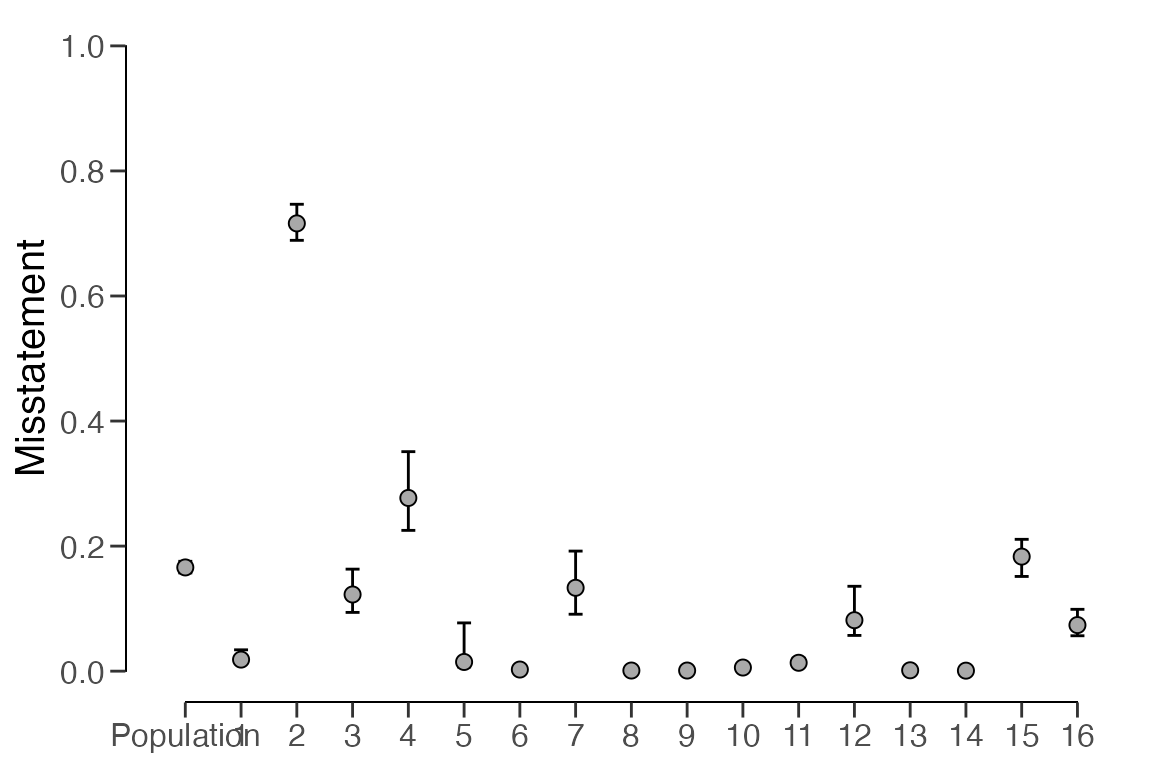

## 20 4000 15 3 3 0.20000 0.07266 0.45646 0.25646In this scenario, the output of the summary() function

indicates that the estimated misstatement in the population is 5.98

percent, with the 95 percent (two-sided) credible interval extending

from 4.28 percent to 8.22 percent. The estimates for each stratum vary

significantly from one another but exhibit relative uncertainty. They

can be visualized via the call below to

plot(..., type = "estimates")

plot(result_np, type = "estimates")

The prior and posterior distribution for the population misstatement

can be obtained using the plot(..., type = "posterior")

function.

plot(result_np, type = "posterior")

Approach 2: Partial pooling

The partial pooling approach (pooling = "partial")

presumes both differences and similarities between strata. This enables

the auditor to share information among the strata to minimize

uncertainty in the population estimate. The following call evaluates the

sample using a Bayesian stratified evaluation procedure, where the

stratum estimates are poststratified to derive the population estimate.

Remember, it is important to set the seed via set.seed() to

make the results reproducible.

set.seed(1)

result_pp <- evaluation(

materiality = 0.05, method = "binomial",

n = retailer[["samples"]], x = retailer[["errors"]],

N.units = retailer[["items"]], pooling = "partial",

alternative = "two.sided", prior = TRUE

)

summary(result_pp)##

## Bayesian Audit Sample Evaluation Summary

##

## Options:

## Confidence level: 0.95

## Population size: 144000

## Materiality: 0.05

## Hypotheses: H₀: Θ = 0.05 vs. H₁: Θ ≠ 0.05

## Method: binomial

## Prior distribution: Nonparametric

##

## Data:

## Sample size: 2575

## Number of errors: 115

## Sum of taints: 115

##

## Results:

## Posterior distribution: Nonparametric

## Most likely error: 0.0423

## 95 percent credible interval: [0.032494, 0.053654]

## Precision: 0.011354

## BF₁₀: 0.030086

##

## Strata (20):

## N n x t mle lb ub precision

## 1 5000 300 21 21 0.0579 0.04003 0.08836 0.03046

## 2 5000 300 16 16 0.0503 0.03217 0.07359 0.02329

## 3 5000 300 15 15 0.0424 0.03042 0.07060 0.02820

## 4 5000 300 14 14 0.0425 0.02849 0.06764 0.02514

## 5 5000 300 16 16 0.0437 0.03195 0.07382 0.03012

## 6 5000 150 5 5 0.0378 0.01823 0.06365 0.02585

## 7 5000 150 4 4 0.0360 0.01511 0.05944 0.02344

## 8 5000 150 3 3 0.0341 0.01177 0.05539 0.02129

## 9 5000 150 4 4 0.0364 0.01474 0.05940 0.02300

## 10 5000 150 5 5 0.0357 0.01783 0.06357 0.02787

## 11 10000 50 2 2 0.0433 0.01658 0.08010 0.03680

## 12 10000 50 3 3 0.0431 0.02147 0.09121 0.04811

## 13 10000 50 2 2 0.0373 0.01676 0.07932 0.04202

## 14 10000 50 1 1 0.0356 0.01120 0.07089 0.03529

## 15 10000 50 0 0 0.0392 0.00548 0.06181 0.02261

## 16 10000 15 0 0 0.0364 0.00895 0.08006 0.04366

## 17 10000 15 0 0 0.0374 0.00861 0.07943 0.04203

## 18 10000 15 0 0 0.0387 0.00867 0.08028 0.04158

## 19 10000 15 1 1 0.0403 0.01598 0.09819 0.05789

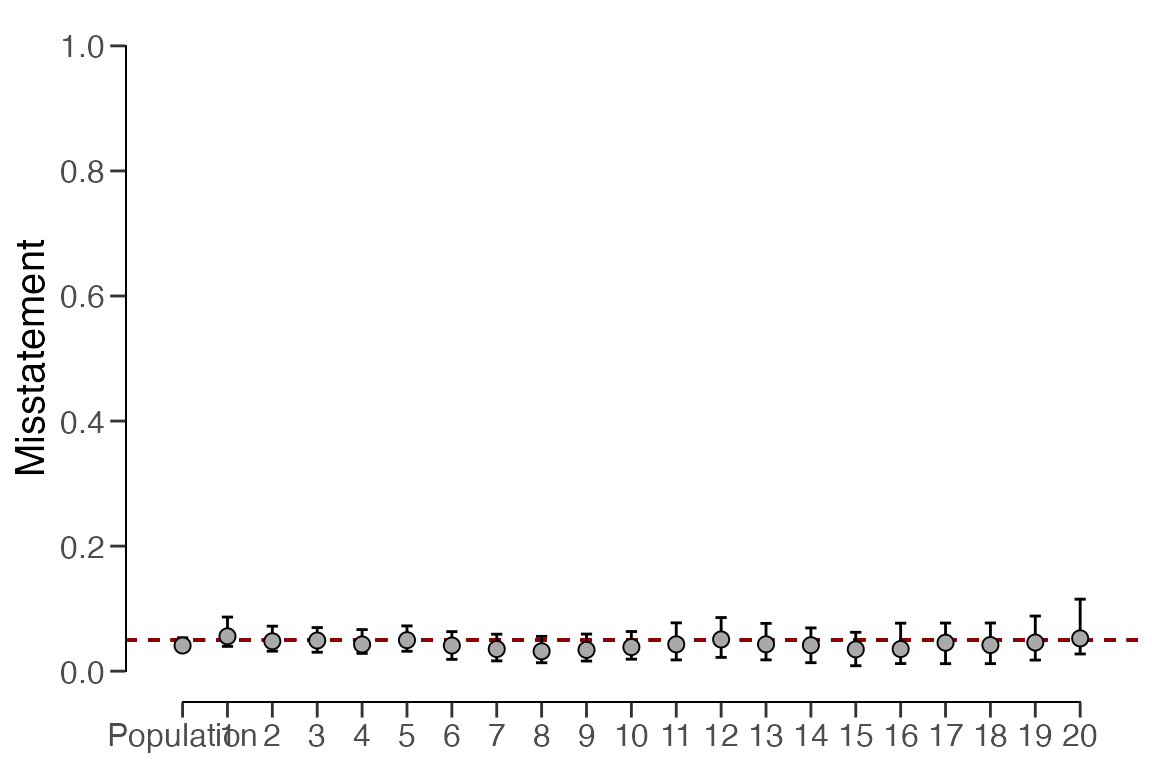

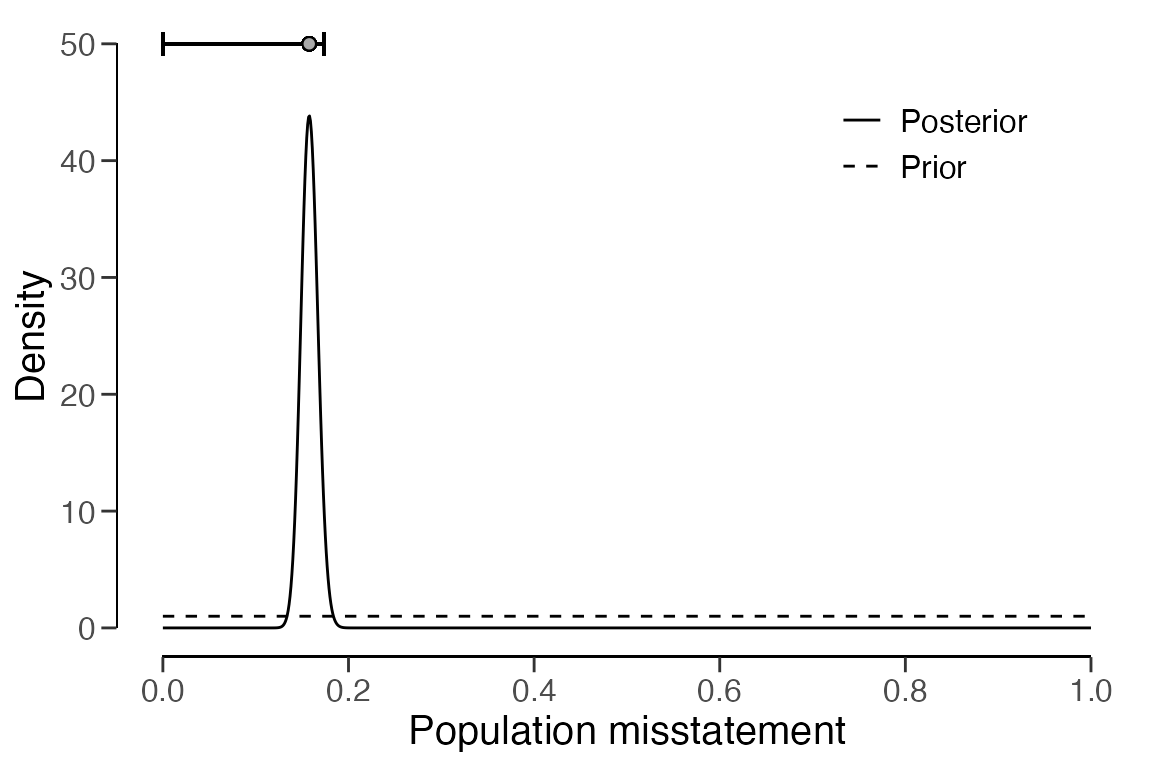

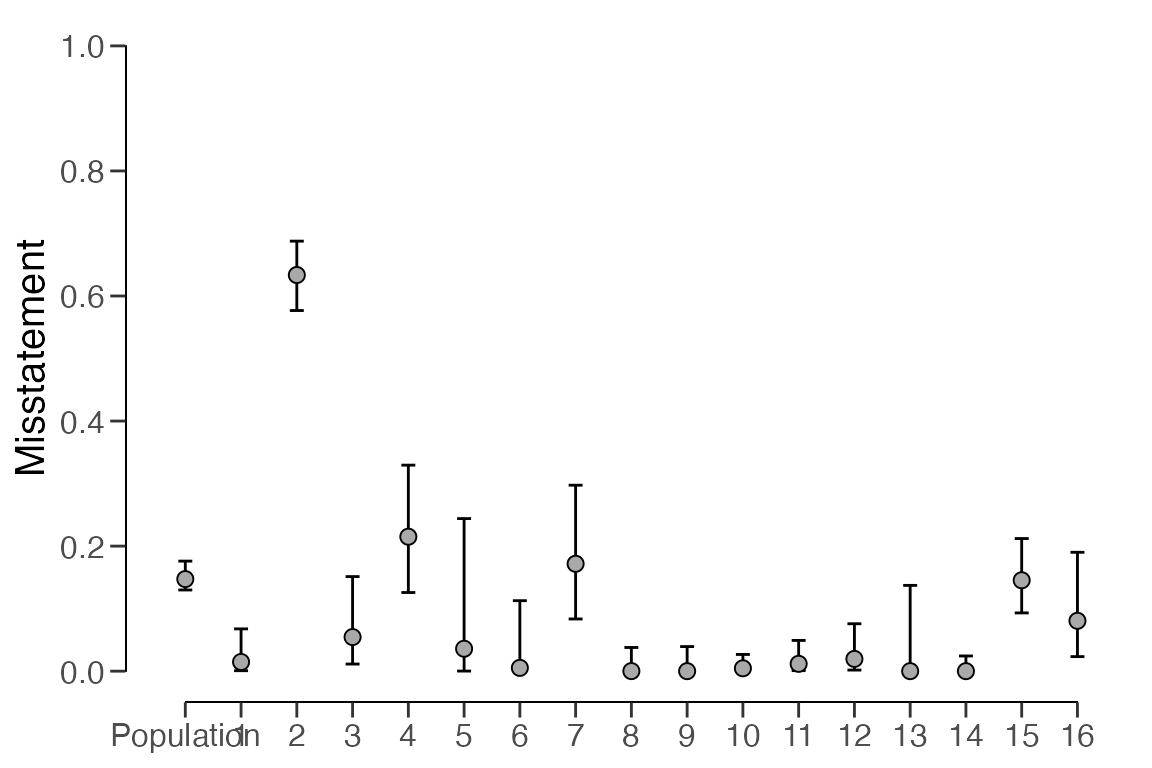

## 20 4000 15 3 3 0.0472 0.02772 0.13675 0.08955In this scenario, the output indicates that the estimated

misstatement in the population is 4.23 percent, with the 95 percent

credible interval extending from 3.25 percent to 5.37 percent. Note that

this population estimate is considerably less uncertain compared to the

no pooling approach. Similarly to the no pooling approach, the stratum

estimates differ from each other but are closer together and exhibit

less uncertainty. This can be explained by the fact that the partial

pooling approach allows for information to be shared between strata. The

stratum estimates can be visualized via a call to

plot(..., type = "estimates").

plot(result_pp, type = "estimates")

The prior and posterior distribution for the population misstatement

can be obtained using the plot(..., type = "posterior")

function.

plot(result_pp, type = "posterior")

Evaluation using data

We now consider the situation where the auditor has access to the sample (and potentially the population) data and wants to perform inference about the misstatement using these data.

Non-stratified samples

In this example, we will demonstrate how to evaluate a non-stratified

sample using a data set. For this, we will use the accounts

data that is included in the package. These data represent an audit

sample obtained from a population of

= 87 accounts receivable, totaling $612,824 in book value (Higgins & Nandram, 2009; Lohr, 2021).

## account bookValue auditValue

## 1 3 6842 6842

## 2 9 16350 16350

## 3 13 3935 3935

## 4 24 7090 7050

## 5 29 5533 5533

## 6 34 2163 2163To evaluate a non-stratified sample using data, you need to specify

the data, values, and

values.audit arguments in the evaluation()

function. The input for the latter two arguments should be the name of

the corresponding column in the input for the data

argument. In the accounts data, these two columns are

called bookValue and auditValue,

respectively.

Classical approach

The command below evaluates the allowances sample using

a classical non-stratified evaluation approach.

evaluation(

data = accounts, method = "binomial",

values = "bookValue", values.audit = "auditValue"

)##

## Classical Audit Sample Evaluation

##

## data: accounts

## number of errors = 4, number of samples = 20, taint = 0.16127

## 95 percent confidence interval:

## 0.0000000 0.1527346

## most likely estimate:

## 0.0080633

## results obtained via method 'binomial'In this instance, the output indicates that the estimated most likely

misstatement in the population is 0.81 percent. The 95 percent

(one-sided) confidence interval extends from 0 percent to 15.27 percent.

More detailed information about the results can be obtained via the

summary() function.

Bayesian approach

The call below evaluates the accounts sample using a

Bayesian non-stratified evaluation procedure.

result <- evaluation(

data = accounts, method = "binomial",

values = "bookValue", values.audit = "auditValue", prior = TRUE

)

print(result)##

## Bayesian Audit Sample Evaluation

##

## data: accounts

## number of errors = 4, number of samples = 20, taint = 0.16127

## 95 percent credible interval:

## 0.000000 0.145994

## most likely estimate:

## 0.0080633

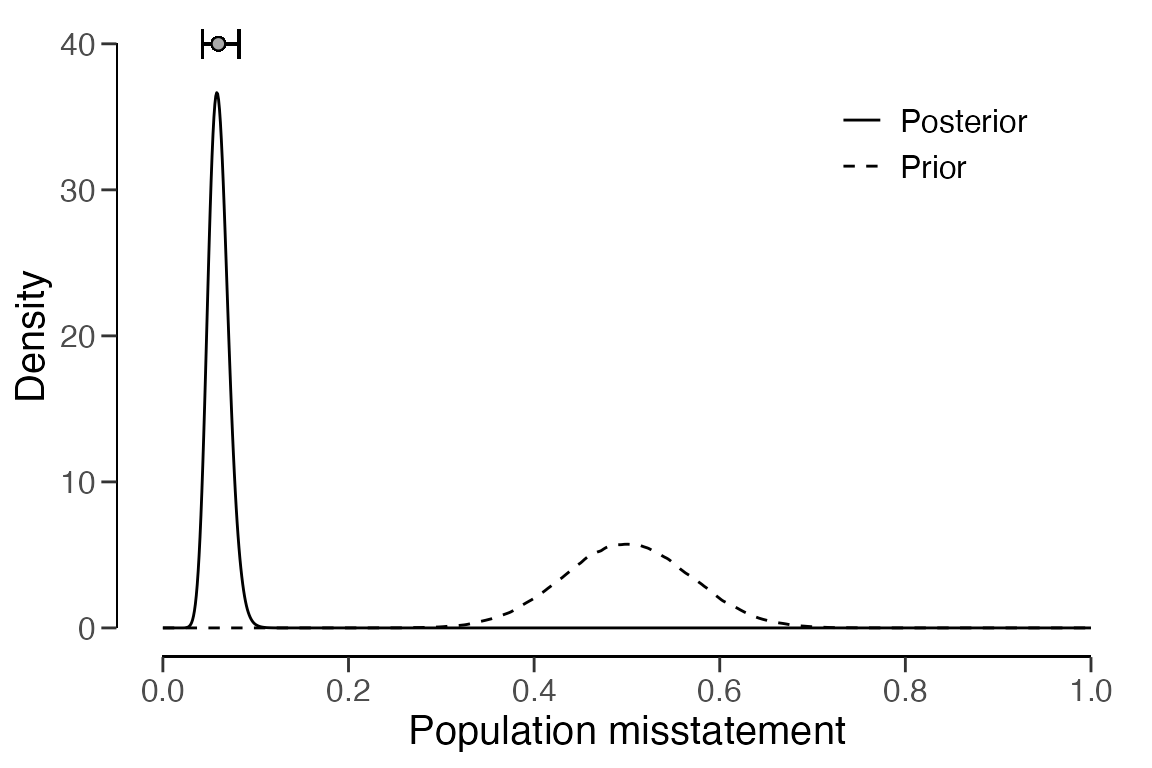

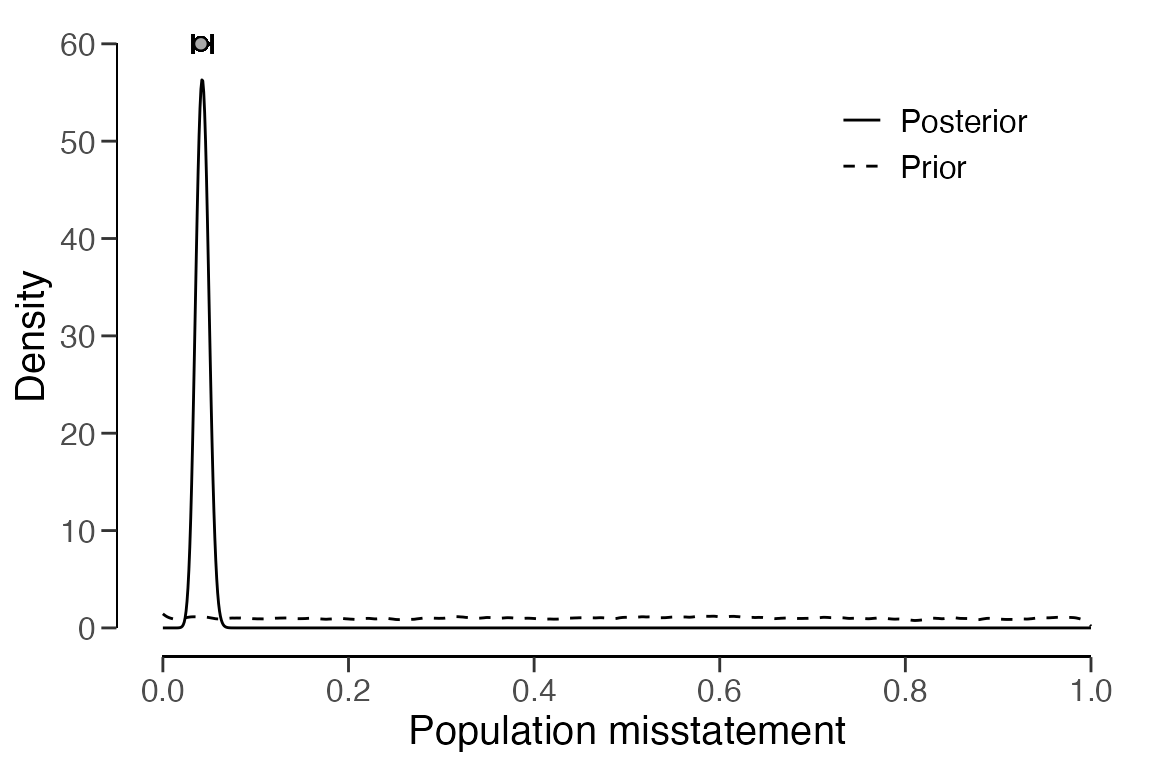

## results obtained via method 'binomial' + 'prior'The output shows that the estimate of the misstatement in the

population is again 0.81 percent, with the 95 percent (one-sided)

credible interval ranging from 0 percent to 14.6 percent. For the

Bayesian analysis, the prior and posterior distribution can be

visualized by a call to plot(..., type = "posterior").

plot(result, type = "posterior")

You can also quantify and monitor evidence for or against the claim that the misstatement is lower than a specific performance materiality using the Bayes factor. Suppose that the performance materiality for this example is set to ten percent of the population value. It is recommended to use an impartial prior distribution when calculating the Bayes factor, which can be set up using the code below.

prior <- auditPrior(

materiality = 0.1, method = "impartial", likelihood = "binomial"

)After it has been specified, you can use the impartial prior

distribution in the evaluation() function as input for the

prior argument.

result <- evaluation(

materiality = 0.1, data = accounts, method = "binomial",

values = "bookValue", values.audit = "auditValue", prior = prior

)

print(result)##

## Bayesian Audit Sample Evaluation

##

## data: accounts

## number of errors = 4, number of samples = 20, taint = 0.16127, BF₁₀ =

## 11.274

## alternative hypothesis: true misstatement rate is less than 0.1

## 95 percent credible interval:

## 0.0000000 0.1171385

## most likely estimate:

## 0.0063047

## results obtained via method 'binomial' + 'prior'It can be seen from the output that the Bayes factor in favor of the

hypothesis of tolerable misstatement is 11.274. This indicates that the

data is roughly 11 times more likely under the hypothesis of tolerable

misstatement than under the hypothesis of intolerable misstatement.

Besides computing the Bayes factor for the total sample, it is also

possible to see how the Bayes factor evolves as a function of the sample

size. This can be done via a call to

plot(..., type = "sequential").

plot(result, type = "sequential")

Stratified samples

In this example, we will demonstrate how to evaluate a stratified

sample using a data set. We will use the allowances data

set that is included in the package. This data set comprises

= 3500 subsidy declarations from municipalities. Each line item has a

recorded value book value (column bookValue) and an audited

value (column auditValue), which is the true value for the

purpose of this illustration. The data set already identifies the items

that have been audited as part of the sample in the column

times. In this scenario, we will only be performing

estimation and therefore do not specify the materiality

argument in the evaluation() function.

## item branch bookValue auditValue times

## 1 1 12 1600 1600 1

## 2 2 12 1625 NA 0

## 3 3 12 1775 NA 0

## 4 4 12 1250 1250 1

## 5 5 12 1400 NA 0

## 6 6 12 1190 NA 0To evaluate a stratified sample using a data set, you need to specify

the data, values, values.audit,

and strata arguments in the evaluation()

function. The input for N.units is once again optional. In

this example, the units are monetary, determined by summing up the book

values of the items within each stratum. For instance, we can see that

stratum two is the largest, with a total value of $2,792,814.33 and

stratum five is the smallest, with a total value of $96,660.53.

N.units <- aggregate(allowances$bookValue, list(allowances$branch), sum)$x

print(data.frame(N.units))## N.units

## 1 317200.09

## 2 2792814.33

## 3 1144231.69

## 4 414202.89

## 5 96660.53

## 6 348006.13

## 7 2384079.33

## 8 1840399.33

## 9 563957.70

## 10 3198877.73

## 11 1983299.06

## 12 319144.13

## 13 148905.79

## 14 513058.76

## 15 432007.61

## 16 275403.70Classical approach

The following command evaluates the allowances sample

using a classical stratified evaluation method. In this process, the

estimates from each stratum are poststratified to derive the estimate

for the entire population. Note that for computational reasons it is

important to set a seed here via set.seed(). Furthermore,

note that the sample is automatically separated from the population

because the times value for items not in the sample is

0.

set.seed(1)

result <- evaluation(

data = allowances, times = "times", method = "binomial",

values = "bookValue", values.audit = "auditValue",

N.units = N.units, strata = "branch",

alternative = "two.sided"

)

print(result)##

## Classical Audit Sample Evaluation

##

## data: allowances

## number of errors = 401, number of samples = 1604, taint = 252.93

## 95 percent confidence interval:

## 0.1298437 0.1759994

## most likely estimate:

## 0.14723

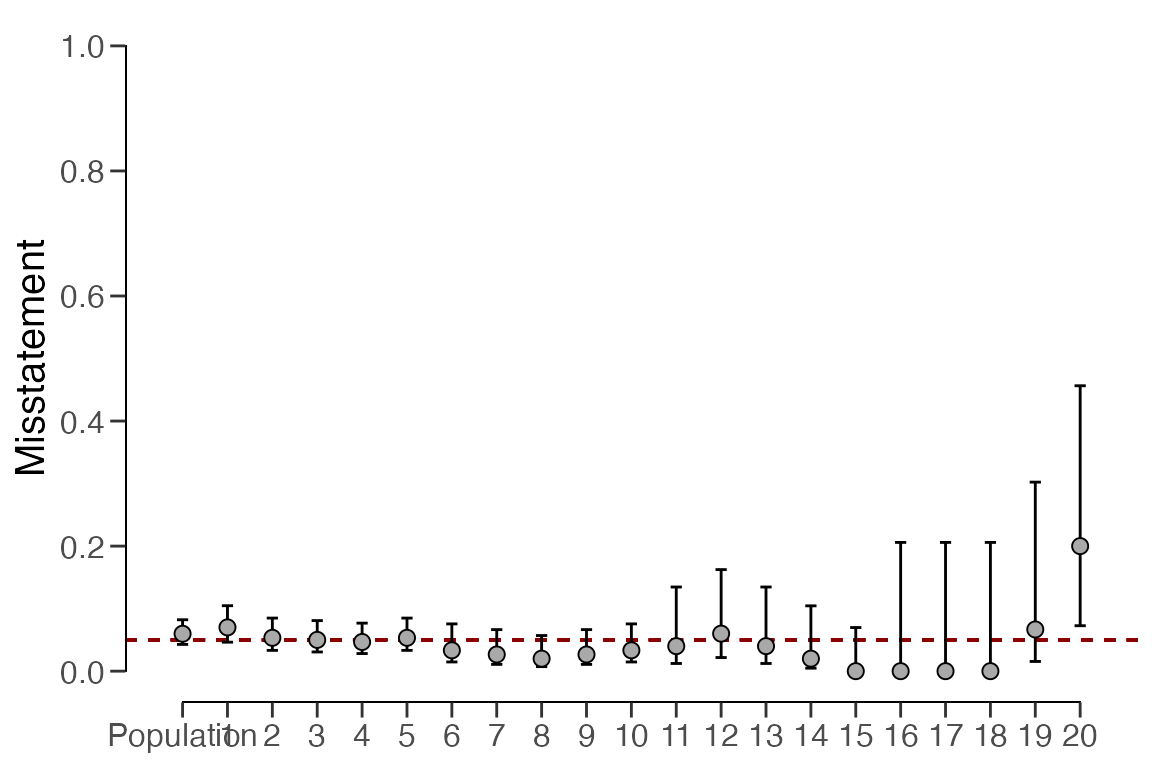

## results obtained via method 'binomial' + 'no-pooling'In this instance, the output reveals that the estimated misstatement

in the population is 14.72 percent. The 95 percent confidence interval

spans from 12.98 percent to 17.6 percent. The precision of the

population estimate is therefore 4.26 percent. The estimates for each

stratum are visualized below. For more detailed information, including

the actual stratum estimates, you can use the summary()

function.

plot(result, type = "estimates")

Bayesian approach

Bayesian inference can enhance the estimates obtained from the

classical approach by pooling information across strata where feasible.

The following command evaluates the allowances sample using

a Bayesian stratified evaluation method. In this process, the estimates

from each stratum are pooled and poststratified to derive the estimate

for the entire population.

set.seed(1)

result <- evaluation(

data = allowances, times = "times", method = "binomial",

values = "bookValue", values.audit = "auditValue",

N.units = N.units, strata = "branch", pooling = "partial",

alternative = "two.sided",

prior = TRUE

)

print(result)##

## Bayesian Audit Sample Evaluation

##

## data: allowances

## number of errors = 401, number of samples = 1350, taint = 224.66

## 95 percent credible interval:

## 0.1571337 0.1757009

## most likely estimate:

## 0.1659

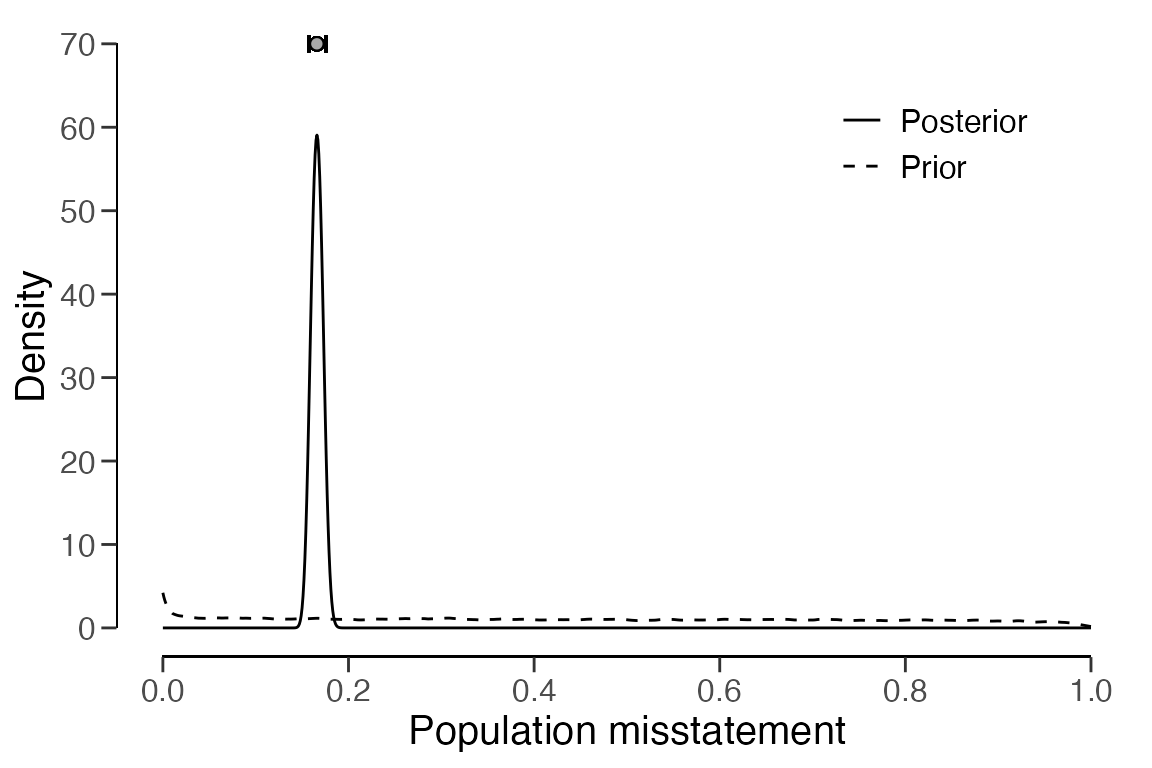

## results obtained via method 'binomial' + 'partial-pooling' + 'prior'The output indicates that the estimated misstatement in the

population is 16.59 percent. The 95 percent credible interval spans from

15.71 percent to 17.57 percent. The precision of the population estimate

is therefore 1.86 percent, which is lower than that of the classical

approach. The estimates for each stratum are visualized below using the

plot(..., type = "estimates) command but their actual

values can be once again be obtained using the summary()

function.

plot(result, type = "estimates")

The prior and posterior distribution for the population misstatement

can be obtained via the plot(..., type = "posterior")

function.

plot(result, type = "posterior")